by SFT | Jul 12, 2026 | Financial Planning, St Francis

At Client Care, we’re always glad to meet new people. We love what we do, and there’s a particular kind of satisfaction that comes from helping someone retire comfortably, with dignity, and then go on to live their best life, by choice, rather than by chance.

After more than thirty years in this business, we’re fortunate that most of our new clients find us through referrals – from existing clients, and even from people who’ve never worked with us but know, through others, that we can be trusted.

We recently met a new couple, referred by a mutual friend. They’ve been together since their early twenties, and over the last twenty-five years, they’ve built a successful business from scratch and raised a family. They’re now at the stage where they can save more meaningfully and start thinking properly about the next chapter of their lives.

Many people, looking at what this couple has achieved, might assume that planning out their last working decade should come naturally to them. After all, how hard can it be?

The truth is, they could certainly try to go it alone. But their years in business have taught them something valuable: asking for help is usually cheaper, in the end, than wandering into territory you don’t fully understand.

We see this pattern often. People come to us out of a quiet fear that they’ve left things too late. In our experience, it very seldom is.

Our process starts by helping clients understand exactly where they stand today, and then mapping out how to get to where they want to be. Every person walks their own road, so every financial plan should speak to their life and their particular story.

Yes, the numbers have to add up. But over a retirement that might stretch across thirty-five years, there are many levers that can be pulled to shape the outcome someone wants. And that outcome needs to reflect personal values – the things that matter most to them. Some people live for travel. Others live for their sport. Almost everyone will do anything for their family.

These softer questions are, in truth, the most important part of the plan. It’s easy to miss this if you’re working with an adviser who only does the numbers. The numbers, honestly, are the easy part. Good retirement planning gets that right, but it also pays close attention to the human side.

If your numbers look fine but something still feels like it’s missing, chances are we can help. Pop in for a chat.

—

Dirk Groeneveld, Certified Financial Planner

t. 083 261 9287

e. dirk@clientcare.co.za

An Investment Portfolio Without a Plan is Meaningless

Five Dangers Of DIY Financial Planning

Finding The Delicate Balance In Giving

Dead Money, Living Money

—

Disclaimer:

This article is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Client Care and PWM and its directors, officers, and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of, or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this article.

by SFT | Jul 5, 2026 | Financial Planning, St Francis

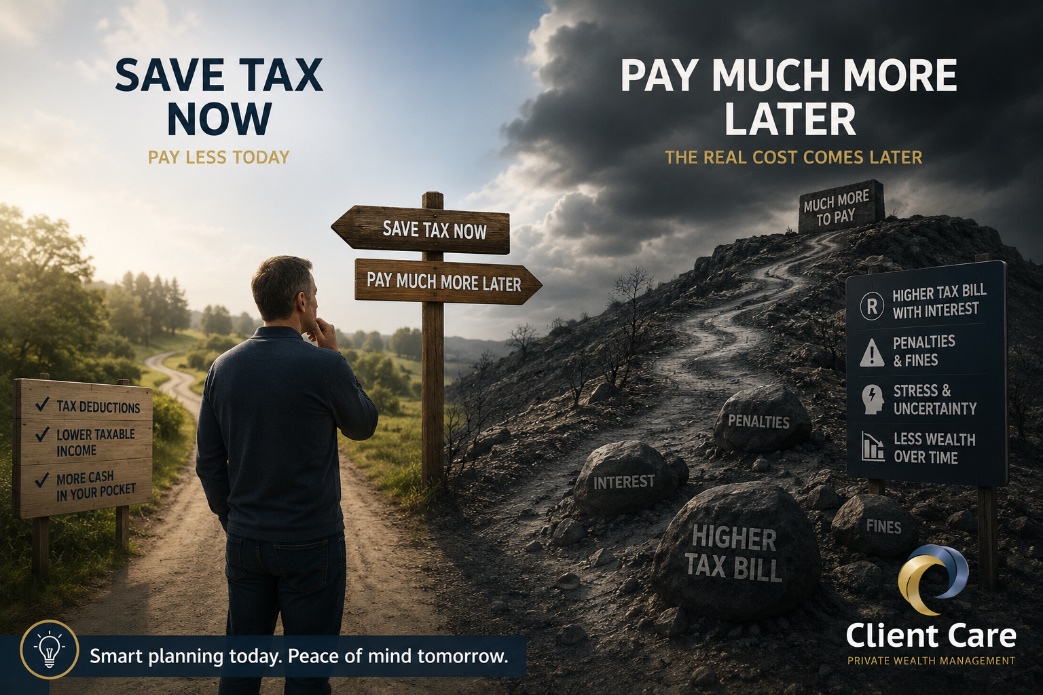

Every so often someone tells me, quite proudly, that they don’t really need a financial planner. They’ve done well on their own, they say, and they’d rather not pay for advice they might not use. I always understand where this comes from. A few people genuinely can manage on their own. But in over thirty years of doing this work, I’ve seen far more often that the “DIY” route ends up costing people far more than any advice fee ever would.

Three recent conversations illustrate this beautifully.

The first was with a retired accountant who told me, with some satisfaction, that he hadn’t paid tax in seven years. He’d lived off cash and unit trusts, flipping the odd property along the way. It sounded clever – until we looked closer. All that was left was a preservation fund, and now he has no choice but to pay a hefty upfront tax on any lump sum, or over 35% tax on the income he needs to maintain his lifestyle. Avoiding tax for seven years has landed him with a far bigger bill today.

The second was a lady who sold part of her business for more money than she could ever spend. Nervous about markets, and convinced a crash was coming, she has sat in cash for three years. Every year the interest has triggered a large tax bill, while the market she avoided has grown by roughly 50%. She has, in real terms, saved herself poorer.

The third was an English gentleman who fell in love with St Francis Bay, made it his home, and became a South African taxpayer as a result. We discussed moving his investments into a proper tax-efficient wrapper – one that would also solve several estate planning headaches. He chose to go it alone instead. The result: a capital gains tax bill of around R6 million on his roughly R100 million portfolio. Had he restructured, that cost would look trivial next to the tax he’ll save over the rest of his life.

None of these were foolish people. Quite the opposite – each was capable, successful, and confident. That’s often exactly the trap. Confidence in one area of life doesn’t always translate into expertise in tax and estate planning.

Good advice rarely feels dramatic in the moment. But as these three stories show, its absence certainly can be.

—

Dirk Groeneveld, Certified Financial Planner

t. 083 261 9287

e. dirk@clientcare.co.za

An Investment Portfolio Without a Plan is Meaningless

Five Dangers Of DIY Financial Planning

Finding The Delicate Balance In Giving

Dead Money, Living Money

—

Disclaimer:

This article is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Client Care and PWM and its directors, officers, and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of, or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this article.

by SFT | Jun 22, 2026 | Financial Planning, St Francis

I am writing this from a bush camp deep in Gonarezhou, Zimbabwe, somewhere past the halfway mark of a ten-day trip with a small group of friends. Already, enough has gone sideways to remind me just how much planning a trip like this has in common with planning a retirement.

This trip was planned well in advance. Not years, like a retirement, but if you scale it to the length of the trip, the ratio is remarkably similar. We had to decide where to go and what kind of accommodation we wanted, weighing options at different price points until we found our ideal “digs” within budget. Securing the booking, the right dates, the right camps was a challenge in its own right. We also had to choose who would join us. Not a simple decision, because the wrong mix of people can sour an experience that the scenery alone cannot save. As it happened, one couple had to withdraw closer to the time for very good personal reasons, opening a space for someone new to the group whom we had never met, but who came highly recommended by others in our travel group.

In the weeks before departure, vehicles and caravans were serviced and packed, meals were planned. We had to order meat in Zimbabwe, due to foot-and-mouth restrictions back home, from butcheries we had never used in towns we had never visited. Research was done. Orders were placed. Fuel budgets shifted almost daily as the Iran-US conflict rattled prices and availability. Everything we could plan for was done.

Then we set off, and the plan immediately met reality.

Our meat orders turned out to be enormous by South African standards, I am fairly sure my lamb ribs came from an Eland, and our fridges and freezers had to be repacked on the fly. A welcome problem, simply solved with having more braais than scheduled. Then the “safe” route into the park took more than double the time we expected, complete with some properly extreme 4×4 driving. One member’s brand-new, beautifully engineered bush caravan lost a wheel four kilometres from camp, costing us three hours and a dark arrival. Thankfully we had three engineers in the group, so a recovery vehicle was never needed.

The real lesson came at the Runde River causeway crossing. We had done a practice run the day before with no caravans, and it went smoothly. We reasoned the river would only keep subsiding, so the next day’s crossing should be easier still. We were wrong. The river had risen overnight. My carefully discussed strategy, enter slowly, accelerate once it deepens, got me and my caravan stuck in fine sand 200 metres in. It took a friend and his vehicle behind me several attempts to tow us back out. My second attempt used the opposite approach, more speed, more commitment, and it worked.

This is the thread I keep returning to; no matter how much we plan, research and strategise, things rarely go exactly to plan. When they don’t, we lean on the people we have chosen to travel with, and they lean on us in turn.

It strikes me that this ten-day trip took hours of careful planning, yet I regularly meet people who spend far less time planning thirty or forty years of retirement, and who leave that planning too late. Planning retirement alone is difficult, arguably impossible to do well.

That is exactly where we at Client Care Private Wealth Management come in, not only to help with the planning long before the event, but to walk the road with you through it, helping when the unexpected happens, towing you out when you get stuck, and making sure you live a retirement that is dignified and free.

It’s never too late to choose who to walk your path with.

Dirk Groeneveld, Certified Financial Planner

t. 083 261 9287

e. dirk@clientcare.co.za

An Investment Portfolio Without a Plan is Meaningless

Five Dangers Of DIY Financial Planning

Finding The Delicate Balance In Giving

Dead Money, Living Money

—

Disclaimer:

This article is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Client Care and PWM and its directors, officers, and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of, or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this article.

by SFT | Jun 14, 2026 | Financial Planning, St Francis

The global stock market, shares in the great companies of the world, is one of the most powerful wealth-building tools we have. A recent study looked at every meaningful listed company across 43 countries from 1990 to 2020 and found that global markets created around $76 trillion more wealth for shareholders than cash would have over the same period.

Here’s the surprising part. That wealth did not come from the market broadly. More than half of the 64,000 companies studied actually returned less than cash over their lifetimes. Almost all the net wealth created came from just 2.4% of companies.

So how does an ordinary investor get a slice of that 2.4%?

There seem to be two routes. The first is to try to identify those winners ahead of time. This is what much of the investment industry is built around, clever people, deep research, sophisticated models, all hunting for the same small group of exceptional companies. Yet the evidence is sobering. Most professional fund managers underperform the broad market over long periods, and even among those who do beat it, separating genuine skill from plain luck is notoriously difficult. Picking winners in advance is, for almost everyone, a losing game.

The second route is far simpler: buy the whole haystack instead of hunting for the needle.

A globally diversified fund holds every listed company of any real size. The next Apple, Microsoft or Nvidia is already in there somewhere, sitting alongside thousands of companies that will go nowhere. You don’t need to know which is which, you own them all, and so you automatically own the winners too.

This kind of fund has no opinion about whether a share is too expensive. It holds the big companies simply because they are big and keeps holding them as they grow bigger still. A skilled stock-picker might have sold Apple back in 2010, convinced it had already had its run. A broad index fund could never do that, it doesn’t form opinions, and that lack of opinion is precisely what keeps you riding the winners for as long as they keep winning.

None of this is a free ride, though. Owning the whole market means owning every downturn along with every winner. The reward only comes to investors who can stay calm and stay invested through the inevitable rough patches.

And this is really the heart of it. A good portfolio is only one part of a good outcome. A sound long-term plan, and the discipline to hold steady when markets wobble, matter every bit as much as the funds you hold. Behaviour, more than selection, tends to decide who does well over time.

So, ask yourself; are you, or whoever manages your money, trying to guess which companies will end up in that magic 2.4%? Or are you simply happy to own all of them?

Owning the haystack is the easy part. Building a plan around it, and having someone alongside you when markets get uncomfortable, is where the real value lies. If you’d like to talk through what that could look like for you, I’d be glad to have that conversation.

—

Dirk Groeneveld, Certified Financial Planner

t. 083 261 9287

e. dirk@clientcare.co.za

An Investment Portfolio Without a Plan is Meaningless

Five Dangers Of DIY Financial Planning

Finding The Delicate Balance In Giving

Dead Money, Living Money

—

Disclaimer:

This article is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Client Care and PWM and its directors, officers, and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of, or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this article.

by SFT | Jun 7, 2026 | Financial Planning, St Francis

All Small-Scale Embedded Generation (SSEG) systems must be authorised by Kouga Local Municipality before installation. This requirement helps ensure that systems are safe, compliant, and legally connected to the municipal electricity network.

SSEG systems include solar photovoltaic (PV) installations, battery-only storage systems, and alternative energy technologies such as wind, biogas, generator, and micro-hydro systems.

Safety and Compliance

Firstly, municipal registration helps protect both residents and municipal employees. Incorrectly connected or unapproved systems can create serious safety risks, including electrocution and fire hazards.

In addition, unregistered systems may affect insurance claims if damage or accidents occur. For this reason, residents are encouraged to ensure that all systems meet the required safety and compliance standards before use.

Supporting the Electricity Network

At the same time, proper registration helps the municipality manage the electricity network more effectively as more households adopt self-generation solutions.

Unregistered systems can place additional pressure on the grid and may affect the reliability and stability of electricity supply in surrounding areas. Authorised systems therefore support better planning, monitoring, and long-term network management.

Work With Qualified Installers

Residents should work with qualified installers who understand municipal compliance requirements. Furthermore, homeowners are encouraged to confirm that quotations and service agreements include all required documentation, testing, and certification costs.

Importantly, registration and authorisation through the municipality are free of charge. However, installers or third-party service providers may charge professional fees to assist with applications and compliance processes.

By registering SSEG systems correctly, residents contribute to a safer, more reliable, and better-managed electricity network across the Kouga region.

by SFT | Jun 7, 2026 | Financial Planning, St Francis

Budget! A word feared in most households.

One of the biggest causes of arguments in households is money. We battle to speak about it, so we push it to the side to be discussed another day. Of all money subjects, a budget is the most important yet neglected tool we should all use.

It is easy to see a budget as something negative, restrictive, controlling, and even untrusting. But if we view it differently, it can be the base on which we build the current and future lives we want. When we want to build a business, a house, buy a car, or go on holiday, we start with a budget which reveals certain options or possibilities to us.

Personal or Household Budget

In a similar way, we should have a personal or household budget which covers fixed and lifestyle expenses, including short- and long-term savings. This budget must not be more than the family income, or it will not work or give a sustainable outcome. Having a budget which we stick to will, instead of making us fearful, give us a feeling of control and allow us to feel positive about the future.

If your financial planner has not asked you to do a budget, let alone update it annually, then you should question how they can give you the advice you need currently, let alone plan for your future retirement. At Client Care, we assist our clients in creating their personal budget in their current positions, as well as what it will look like in retirement. We use cashflow modelling to show what their future outcomes are and then help them understand the trade-offs they can make either now or in the future to make their personal plan work.

If you do not use budgeting, you simply cannot be in control of your financial life. Don’t know where to start? Give us a shout. It starts with the first step.

Dirk Groeneveld, Certified Financial Planner

t. 083 261 9287

e. dirk@clientcare.co.za

An Investment Portfolio Without a Plan is Meaningless

Five Dangers Of DIY Financial Planning

Finding The Delicate Balance In Giving

Dead Money, Living Money

—

Disclaimer:

This article is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Client Care and PWM and its directors, officers, and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of, or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this article.

Recent Comments